Understanding whether to report your Roth IRA on taxes is crucial for effective financial planning. Many individuals wonder if contributions or withdrawals from their Roth IRA will affect their tax obligations. In this article, we will delve into the details of Roth IRAs, how they are treated in terms of taxes, and the implications of reporting them on your tax return.

Roth IRAs offer unique tax advantages that can significantly benefit your retirement savings. However, the rules surrounding them can be complex and often lead to confusion. By the end of this article, you will have a clear understanding of how to handle your Roth IRA on your tax return and what you need to report to ensure compliance with IRS regulations.

Whether you are a seasoned investor or just starting to save for retirement, knowing how your Roth IRA interacts with taxes is essential. This article will provide you with expert insights, authoritative information, and trustworthy guidance to navigate the tax implications of your Roth IRA effectively.

Table of Contents

- 1. What is a Roth IRA?

- 2. Tax Benefits of Roth IRA

- 3. Reporting Requirements for Roth IRA

- 4. Withdrawals and Taxes

- 5. Contributions and Taxes

- 6. Exceptions to the Rule

- 7. Common Mistakes When Reporting Roth IRA

- 8. Conclusion

1. What is a Roth IRA?

A Roth IRA (Individual Retirement Account) is a type of retirement savings account that allows your money to grow tax-free. Contributions to a Roth IRA are made with after-tax dollars, meaning you pay taxes on the money you contribute, but qualified distributions in retirement are tax-free. This makes Roth IRAs an attractive option for many investors.

Here are some key features of Roth IRAs:

- Contributions are made with after-tax income.

- Qualified withdrawals are tax-free in retirement.

- No required minimum distributions (RMDs) during the account owner's lifetime.

- Contributions can be withdrawn at any time without penalty.

2. Tax Benefits of Roth IRA

The tax benefits of a Roth IRA are significant, making it a popular choice for retirement savings. Here are some advantages:

- Tax-Free Growth: Your investments grow tax-free, allowing for more wealth accumulation over time.

- Tax-Free Withdrawals: Withdrawals during retirement are not subject to income tax, which can help reduce your overall tax burden.

- No RMDs: Unlike traditional IRAs, Roth IRAs do not require you to take minimum distributions at age 72, providing greater flexibility in retirement.

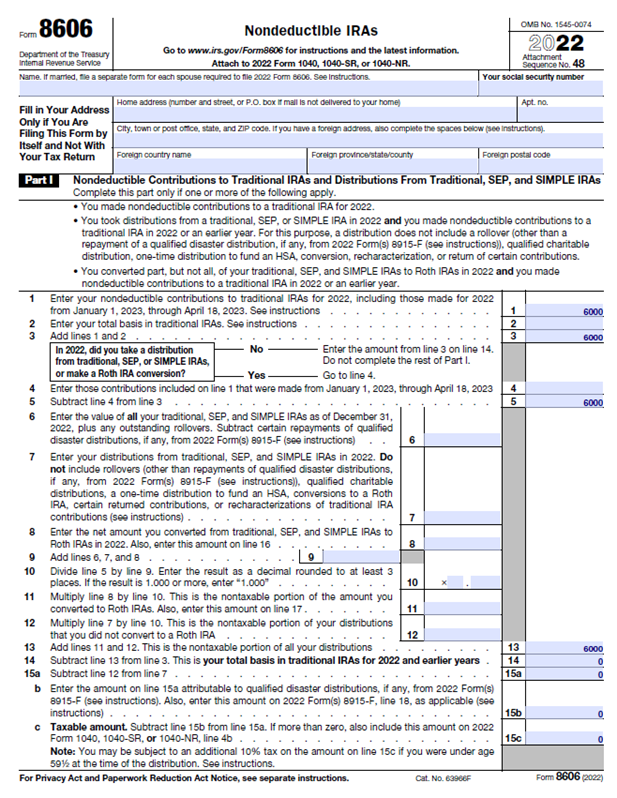

3. Reporting Requirements for Roth IRA

When it comes to reporting your Roth IRA on taxes, the requirements can vary based on your activities within the account. Here are the main points to consider:

3.1 Contributions

You do not need to report your contributions to a Roth IRA on your tax return. However, it is essential to keep track of your contributions to ensure you do not exceed the annual contribution limit set by the IRS.

3.2 Withdrawals

Withdrawals from your Roth IRA may need to be reported on your tax return, depending on the type of withdrawal. If you are taking a qualified distribution, you typically do not need to report it. However, non-qualified distributions may have tax implications.

4. Withdrawals and Taxes

Understanding how withdrawals work in relation to taxes is crucial for effective tax planning. Here's what you need to know:

4.1 Qualified Withdrawals

Qualified withdrawals are tax-free and penalty-free. To be considered qualified, the account must meet the following criteria:

- The account must be at least five years old.

- The account holder must be at least 59½ years old, disabled, or using the funds for a first-time home purchase (up to $10,000).

4.2 Non-Qualified Withdrawals

Non-qualified withdrawals may be subject to taxes and penalties. These withdrawals do not meet the criteria mentioned earlier and may result in the following:

- A 10% early withdrawal penalty.

- Income tax on the earnings portion of the withdrawal.

5. Contributions and Taxes

While contributions to a Roth IRA are not tax-deductible, it is essential to understand how they fit into your overall tax strategy.

5.1 Contribution Limits

The IRS sets annual contribution limits for Roth IRAs, which may change over time. For 2023, the contribution limit is:

- $6,500 for individuals under 50 years old.

- $7,500 for individuals aged 50 and above (catch-up contribution).

5.2 Excess Contributions

If you exceed the contribution limits, you may face penalties. It’s crucial to monitor your contributions carefully to avoid excess penalties:

- A 6% excise tax on the excess contribution each year until it is corrected.

6. Exceptions to the Rule

There are exceptions to the general rules regarding Roth IRAs that can impact your tax reporting. Here are some important exceptions:

6.1 First-Time Home Purchase

As mentioned earlier, you can withdraw up to $10,000 of earnings tax-free for a first-time home purchase if the account has been open for at least five years.

6.2 Disability

If you become disabled, you can withdraw funds from your Roth IRA without incurring penalties, regardless of your age.

7. Common Mistakes When Reporting Roth IRA

Many individuals make mistakes when it comes to reporting their Roth IRA on taxes. Here are some common pitfalls to avoid:

- Failing to track contributions accurately.

- Not understanding the difference between qualified and non-qualified withdrawals.

- Ignoring the contribution limits and facing penalties.

8. Conclusion

In summary, understanding how to report your Roth IRA on taxes is critical for effective tax management and retirement planning. While contributions do not need to be reported, withdrawals may have tax implications depending on their nature. By staying informed and keeping accurate records, you can maximize the benefits of your Roth IRA while minimizing your tax liabilities.

We encourage you to take action by reviewing your Roth IRA contributions and withdrawals to ensure compliance with IRS regulations. If you have any questions or experiences to share, feel free to leave a comment below or explore more articles on our site for additional insights.

Thank you for reading, and we look forward to seeing you back on our site for more valuable financial information!

You Might Also Like

Understanding The Texas FOID Card: A Comprehensive GuideCervical Spinal Cord Cross Section: Understanding The Anatomy And Function

How Much Does A Football Team Cost? A Comprehensive Guide

Healthy Crunchy Snacks: Your Ultimate Guide To Delicious And Nutritious Munchies

Limb Deficiency: Understanding And Navigating Life With Limb Def

Article Recommendations

- The River Century

- How Long Do Tulip Blooms Last

- Healthy Tamale Recipe

- Uncensored Videos

- Hughes Net Bill

- Los Rodeos Airport Tenerife

- April Cancer Horoscope 2024

- Jojo Siwa Real Name

- What Is Corbels

- Sarah Pender

:max_bytes(150000):strip_icc()/savingsvs.ira_V1-b63b805de8554f589543be193cad9857.png)

:max_bytes(150000):strip_icc()/rothira_final-9ddd537c67fd44ecb14dbdeba58a6ace.jpg)