When it comes to understanding insurance policies, the term "deductible" often raises questions among consumers. A $1000 deductible is a common amount seen in many health, auto, and home insurance plans. Understanding what this means can significantly impact your financial decisions and insurance effectiveness. In this article, we will delve deep into the implications of a $1000 deductible, how it works, and what factors to consider when choosing a plan. By the end, you will have a clearer understanding of how deductibles function within the broader context of insurance.

Deductibles are the out-of-pocket costs that policyholders must pay before their insurance coverage kicks in. In simple terms, if you have a $1000 deductible, you are responsible for paying the first $1000 of your claims. This means that if an accident occurs or you need medical care, you will need to cover this amount before your insurer pays for the remainder. Understanding this concept is crucial as it directly affects your potential financial responsibility in the event of a claim.

Furthermore, the choice of deductible can influence your insurance premiums. Typically, higher deductibles lead to lower monthly premiums. However, this balance needs to be carefully considered based on your financial situation, risk tolerance, and the likelihood of needing to make claims. Let’s explore the nuances of a $1000 deductible further and analyze its impact on various types of insurance.

Table of Contents

- What is a Deductible?

- How Does a $1000 Deductible Work?

- Types of Insurance with Deductibles

- Pros and Cons of a $1000 Deductible

- Factors to Consider When Choosing a Deductible

- Impact on Premiums

- Common Misconceptions About Deductibles

- Conclusion

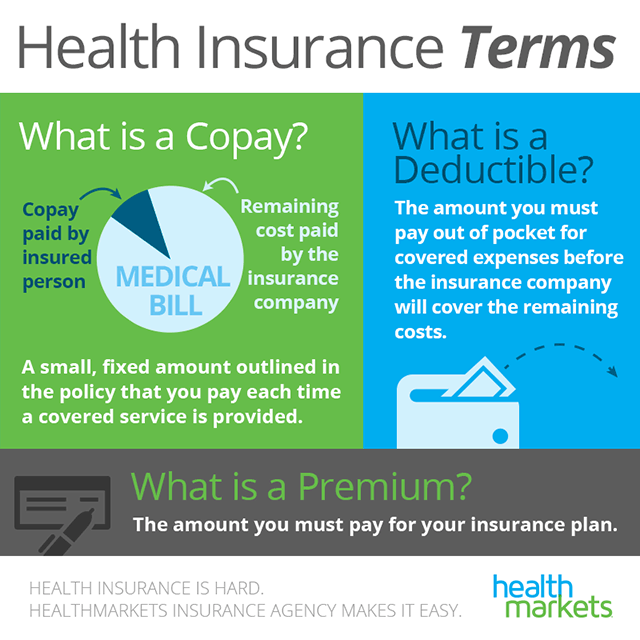

What is a Deductible?

A deductible is the amount of money that a policyholder must pay out-of-pocket before their insurance provider starts to pay for covered expenses. This concept applies to various types of insurance, including health, auto, and homeowners insurance. Deductibles are designed to discourage frivolous claims and encourage responsible risk management.

Types of Deductibles

- Fixed Deductibles: A set dollar amount that must be paid before coverage begins.

- Percentage Deductibles: A percentage of the total cost that must be paid before coverage applies.

- Aggregate Deductibles: The total amount that must be met for all claims within a policy year.

How Does a $1000 Deductible Work?

When you have a $1000 deductible, it means that you will need to pay the first $1000 of any claim before your insurance company begins to pay. For example, if you are in an auto accident that causes $5000 in damages, you would pay $1000, and your insurance would cover the remaining $4000. It is essential to understand that this amount is typically reset annually, meaning you will need to meet this deductible each year before your coverage applies.

Types of Insurance with Deductibles

Deductibles are prevalent in several types of insurance policies. Here are the most common types:

Health Insurance

In health insurance, a $1000 deductible means you must pay $1000 for medical expenses before your insurance begins to cover costs. This can include doctor visits, hospital stays, and prescription medications.

Auto Insurance

For auto insurance, a $1000 deductible means that if you are involved in an accident, you will pay the first $1000 in damages before your insurance covers the rest. This applies to collision and comprehensive coverage.

Homeowners Insurance

In homeowners insurance, a $1000 deductible must be met for claims related to property damage, theft, or liability. This means if a storm damages your roof costing $5000, you will pay $1000, and your insurance will cover the remaining $4000.

Pros and Cons of a $1000 Deductible

Choosing a $1000 deductible has its advantages and disadvantages. Here are some pros and cons to consider:

Pros

- Lower Premiums: Generally, policies with higher deductibles have lower monthly premiums.

- Encourages Responsible Behavior: Higher deductibles can encourage policyholders to be more cautious.

- Potential Savings: If you rarely make claims, you may save money over time.

Cons

- Out-of-Pocket Expenses: You will need to budget for the deductible amount in case of a claim.

- Financial Strain: In the event of a significant claim, coming up with the deductible can be challenging.

- Claim Frequency: If you have frequent claims, a high deductible may not be cost-effective.

Factors to Consider When Choosing a Deductible

When selecting a deductible, it is crucial to consider the following factors:

Your Financial Situation

Evaluate your current financial situation. Can you comfortably pay a $1000 deductible if an unexpected event occurs? If not, you may want to consider a lower deductible.

Your Risk Tolerance

Understanding your risk tolerance is essential. If you are risk-averse, a lower deductible may provide peace of mind, while those comfortable with risk may opt for a higher deductible to save on premiums.

Impact on Premiums

One of the most significant impacts of choosing a $1000 deductible is on your insurance premiums. Generally, the higher the deductible, the lower your premium will be. Here are some insights into this relationship:

- Cost-Benefit Analysis: Determine if the savings on premiums outweigh the potential out-of-pocket costs of a higher deductible.

- Frequency of Claims: If you rarely file claims, a higher deductible might be more beneficial.

- Long-Term Savings: Over time, the savings from lower premiums can add up, even if you have to pay a deductible occasionally.

Common Misconceptions About Deductibles

Many people have misconceptions about deductibles. Here are a few common myths:

Myth 1: The Deductible is the Only Out-of-Pocket Cost

In reality, many insurance policies have additional out-of-pocket costs, such as copayments and coinsurance.

Myth 2: All Claims Require a Deductible

Some claims may not have a deductible, such as certain preventive health services or specific types of coverage.

Conclusion

Understanding what a $1000 deductible means is essential for anyone navigating the world of insurance. It is a critical factor that affects your out-of-pocket expenses and insurance premiums. By weighing the pros and cons, considering your financial situation, and understanding how deductibles work across various types of insurance, you can make informed decisions that align with your financial goals.

If you found this article helpful, please leave a comment below or share it with friends who may benefit from learning more about deductibles and insurance policies. For more insightful articles, be sure to explore our website.

We hope you found this information valuable and encourage you to return for more insights on insurance and financial literacy. Thank you for reading!

You Might Also Like

Mnet Asian Music Awards: A Comprehensive Guide To Asia's Premier Music AwardsComprehensive List Of Malayalam Cinema: A Deep Dive Into The Heart Of Indian Film

Understanding The Effects Of Whip Its: A Comprehensive Guide

Defence Of The Ancients: A Comprehensive Guide To Dota 2

Unlock Amazing Savings With Offers.Greatclips.com Coupons

Article Recommendations

- City Of Summit Nj

- Hughes Net Bill

- 22 Tcm

- Camilla Araujo

- Alice In Wonderland Famous Quotes

- Cast Of Your Place Or Mine

- John Bennett Perry

- Cecelia Name

- Healthy Tamale Recipe

- What Number Was Tony Dorsett

:max_bytes(150000):strip_icc()/What-difference-between-copay-and-deductible_final-bcfbc66f41cc43a6be48dbbe424024e0.png)

.png/9025a687-d4ba-450f-fa19-12a92c3cb212?t=1637254391104&imagePreview=1)